Welcome to WordPress. This is your first post. Edit or delete it, then start writing!

Is ₹5 Lakh Health Insurance Enough in 2026?

You bought a ₹5 lakh health insurance policy five years ago. You paid your premiums on time, never once filed a claim, and felt secure. But then came the hospital bill — and suddenly ₹5 lakh felt like a drop in the ocean.

This is not an exaggerated scenario. It is happening to thousands of Indian families every year. Medical inflation in India has been running at 14–15% annually — nearly double the general inflation rate. What cost ₹2 lakh for a cardiac procedure in 2019 can easily cost ₹4–5 lakh today, and by 2026, that number keeps climbing.

So here is the real question you need to answer: Is ₹5 lakh health insurance actually enough to protect your family in 2026? Let us break it down with actual numbers, real hospital cost data, and an honest assessment that goes beyond the glossy insurance brochures.

The State of Healthcare Costs in India: 2026 Reality Check

Before we dissect the ₹5 lakh cover, we need to understand the medical cost landscape Indians are navigating today. India’s private healthcare sector has undergone a dramatic transformation. Corporate hospital chains have expanded aggressively across Tier 1 and Tier 2 cities, bringing world-class facilities — and world-class price tags — along with them.

According to the National Health Accounts Estimates for India, out-of-pocket expenditure still accounts for nearly 47% of total health spending in the country. This means that despite rising insurance penetration, nearly half of what Indians spend on healthcare comes directly from their pockets. Insurance coverage gaps are a significant reason for this.

Medical inflation compounds the problem. A straightforward hospitalization that cost ₹1.5 lakh in 2019 will conservatively cost ₹2.8–3.2 lakh in 2026. And this is not for complex surgeries — this is for routine hospitalizations. The gap between what people think their insurance covers and what it actually covers has never been wider.

Real Hospital Cost Breakdown: What Procedures Actually Cost in 2026

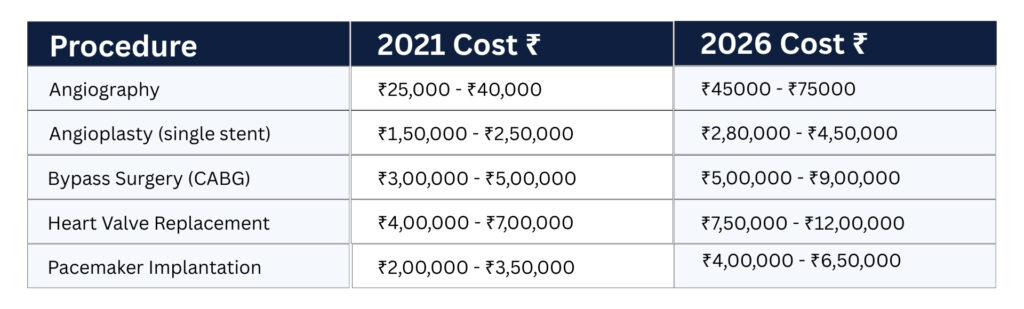

Cardiac Procedures:-

Heart disease is the leading cause of hospitalization claims in India. Here is what you can expect to pay in a reputed private hospital in a metro city:

Notice that a single angioplasty can already breach a ₹5 lakh cover — and that is without factoring in ICU stays, post-operative medications, or follow-up consultations.

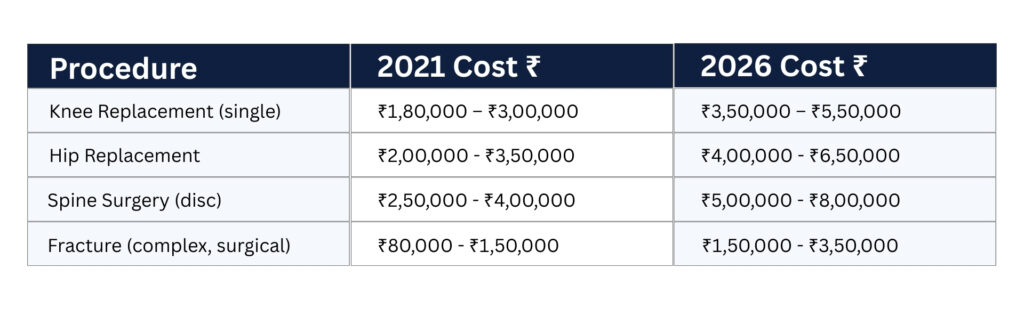

Orthopaedic Procedures :-

With India’s ageing population, joint replacements and fracture treatments have seen massive cost escalations driven by imported implant prices and surgeon fees.

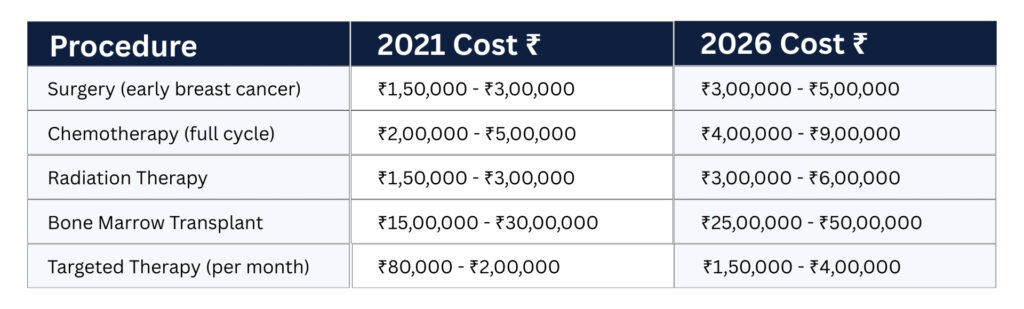

Cancer Treatment:-

Cancer treatment is where insurance gaps become most devastating. The cost of oncology care has exploded, and ₹5 lakh barely covers an early-stage treatment.

A complete cancer treatment cycle — surgery, chemotherapy, radiation, follow-up — can easily run into ₹15–30 lakh or more. A ₹5 lakh cover is not even close to sufficient here.

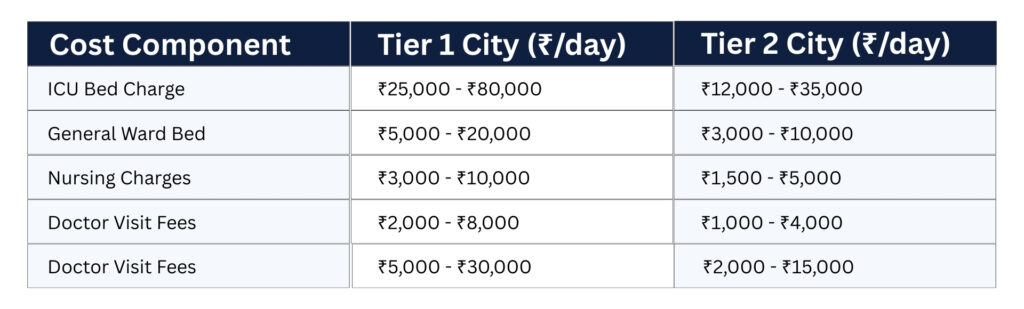

Critical Illness & ICU Costs:-

Beyond surgeries, the hidden cost killer is the Intensive Care Unit. ICU charges at a reputed private hospital in Delhi, Mumbai, or Bengaluru can run ₹25,000–₹80,000 per day. If a patient spends 10 days in the ICU — which is common for serious conditions like stroke, sepsis, or severe COVID complications — that alone can cost ₹5–8 lakh.

The Hidden Costs Your ₹5 Lakh Policy Might Not Cover

Beyond the obvious procedure costs, there are several expense categories that catch policyholders off guard. Many standard health insurance policies have exclusions, sub-limits, and waiting periods that reduce the effective coverage significantly.

Sub-Limits on Room Rent

This is perhaps the most underappreciated trap in Indian health insurance. Many ₹5 lakh policies come with a room rent sub-limit — typically 1% of the sum insured per day, which equals ₹5,000 for a ₹5 lakh policy. If you choose a room that costs ₹8,000 per day, insurers apply proportionate deduction — meaning they reduce all other claims proportionally too, not just the room rent difference. A ₹4 lakh surgery bill can shrink to a ₹2.5 lakh reimbursement.

Pre- and Post-Hospitalization Expenses

Most policies cover only 30–60 days of pre-hospitalization and 60–90 days of post-hospitalization expenses. For chronic conditions like cancer or heart disease, ongoing investigations, medications, and follow-up consultations can far exceed these limits.

Consumables and Non-Medical Expenses

Gloves, syringes, PPE kits, surgical masks, cotton gauze — these ‘consumables’ add up shockingly fast. A 7-day hospitalization can accumulate ₹20,000–₹80,000 in consumables that many standard policies exclude. In 2026, with hospitals increasingly itemizing these charges, this exclusion stings hard.

Modern Treatments and Robotics

Robotic surgery, proton therapy, immunotherapy — these cutting-edge treatments are increasingly becoming the standard of care but are excluded or partially covered by many older policies. Robotic knee replacement can cost 30–40% more than conventional surgery but offers faster recovery. If your policy does not explicitly include modern treatments, you bear the difference.

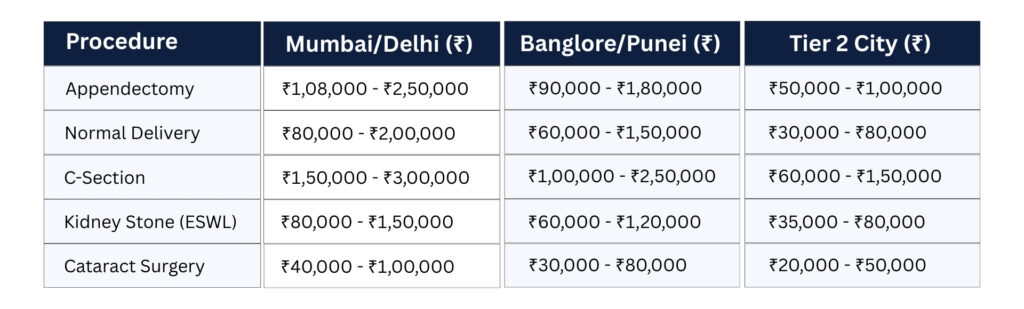

City-Wise Cost Variation: Where You Live Matters

Hospital costs in India are not uniform. Where you live — or where you need to seek treatment — dramatically affects what you pay.

The data makes it clear: if you live in a metro and access care at a corporate hospital, your ₹5 lakh cover evaporates much faster than if you live in a smaller city. This is why blindly relying on any fixed sum insured without accounting for your geography is a significant mistake.

So, Is ₹5 Lakh Enough? The Verdict by Life Stage

The answer is nuanced and depends heavily on who is being covered and at what stage of life.

Young Single Individuals (Age 22–35)

For a healthy individual in their 20s or early 30s with no pre-existing conditions, ₹5 lakh might be just barely adequate for minor hospitalizations, accidents, or common infections. However, even one serious condition — appendicitis with complications, dengue requiring ICU care, or a road accident requiring multiple surgeries — can breach this limit. The risk is low but the consequence of being under-insured is high. Recommended minimum: ₹10–15 lakh.

Young Families with Children

When you add a spouse and children to a floater policy with ₹5 lakh cover, the risk compounds dramatically. Multiple claims in a single year — a maternity complication, a child’s hospitalization, and your own illness — can deplete the cover completely. Given that a C-section alone can cost ₹1.5–3 lakh in a metro, families need significantly higher coverage. Recommended minimum: ₹15–25 lakh family floater.

Middle-Aged Adults (Age 40–55)

This is where the ₹5 lakh cover becomes genuinely dangerous. Lifestyle diseases — hypertension, diabetes, heart conditions — start materializing in this age group, and the treatment costs are significant. A cardiac event at 48 can cost ₹4–8 lakh in hospitalization alone, potentially wiping out a ₹5 lakh cover and leaving a six-figure balance to be paid out of pocket. Recommended minimum: ₹25–50 lakh, ideally with a critical illness rider.

Senior Citizens (Age 60+)

A ₹5 lakh policy for senior citizens is severely insufficient in almost every realistic scenario. The combination of higher claim probability, complex multi-specialty treatments, and longer hospital stays means seniors routinely face bills of ₹3–15 lakh. Additionally, senior citizen premiums are higher and coverage is more restrictive. Recommended minimum: ₹25–50 lakh with comprehensive coverage.

Smart Strategies to Boost Your Coverage Without Breaking the Bank

- Top-Up and Super Top-Up Plans

If buying a fresh ₹25 lakh policy feels prohibitively expensive, a super top-up plan is your best friend. These policies activate above a deductible threshold — say, after the first ₹5 lakh of claims in a year. A ₹20 lakh super top-up with a ₹5 lakh deductible can cost as little as ₹3,000–₹8,000 per year for a 35-year-old. Combined with your existing ₹5 lakh base policy, you now have effective ₹25 lakh coverage at a fraction of the cost.

- Critical Illness Riders or Standalone Policies

Critical illness plans pay a lump sum on diagnosis of specified conditions like cancer, heart attack, kidney failure, or stroke — regardless of actual treatment costs. This lump sum helps cover not just hospital bills but also income loss during recovery, travel for treatment, and lifestyle modifications. A ₹25 lakh critical illness cover can be added for ₹8,000–₹20,000 annually depending on age.

- Choose Policies Without Room Rent Sub-Limits

When renewing or buying a new policy, specifically look for plans that offer no room rent sub-limits or single private AC room as the default entitlement without proportionate deductions. This single feature can make a massive difference in how much of your bill is actually settled.

- Network Hospital Advantage

Always verify that your insurer has tie-ups with quality hospitals in your city. Cashless hospitalization at network hospitals means you do not need to arrange funds upfront — a critical advantage during medical emergencies when time and financial liquidity are both under pressure.

- Annual Cumulative Bonus

Many policies offer a no-claim bonus that increases your sum insured by 10–50% for each claim-free year. A ₹5 lakh policy held for 5 claim-free years could grow to ₹7.5–10 lakh in effective coverage at no additional premium. Factor this into your long-term coverage planning.

How Much Health Insurance Do You Actually Need in 2026?

A simple rule of thumb has emerged among financial planners: your health insurance cover should be at least 50–100 times your monthly income. But an even more practical approach is to benchmark against realistic hospitalization costs in your city.

For a family of four living in a metro city, the minimum recommended coverage in 2026 is ₹25–30 lakh on a floater basis — not ₹5 lakh, and not even ₹10 lakh. For individuals above 45 or with pre-existing conditions, ₹50 lakh in total coverage (base policy plus super top-up) is the new realistic minimum.

The cost of upgrading from ₹5 lakh to ₹25 lakh coverage is far less than most people assume. The incremental premium difference is often just ₹5,000–₹15,000 per year — less than ₹50 per day — but the protection difference is enormous.

The Underinsurance Epidemic in India

Data from the Insurance Regulatory and Development Authority of India (IRDAI) reveals a troubling pattern: a significant portion of health insurance policies sold in India have a sum insured of ₹5 lakh or less. This means millions of Indian families are walking around with a false sense of security — believing they are protected when in reality they are just partially protected.

The consequences of underinsurance are not abstract. They translate into families depleting savings accounts, selling assets, borrowing from relatives, or turning to high-interest personal loans to pay hospital bills. Medical debt is one of the leading causes of financial distress in Indian households, and much of it is avoidable with adequate insurance planning.

The ₹5 lakh cover made sense in 2012. In 2026, given medical cost inflation, it is the equivalent of buying a ₹2 lakh cover fifteen years ago — woefully inadequate for serious health events.

Practical Action Plan: What to Do Right Now

- Review your existing health insurance policy — check the sum insured, sub-limits, exclusions, and waiting periods. Read the fine print, not just the brochure.

- Calculate your realistic risk by estimating the cost of two or three common hospitalizations in your city. If your cover cannot handle two simultaneous claims, you are underinsured.

- Buy a super top-up plan immediately if upgrading your base policy is expensive. It is the most cost-effective way to enhance coverage.

- Add a critical illness plan if you are above 35 or have a family history of heart disease, cancer, or diabetes. The lump sum payout provides financial flexibility that reimbursement plans cannot.

- Choose no-sub-limit plans when renewing. Pay slightly higher premiums for policies that remove room rent caps and cover consumables.

- Revisit your cover annually — not just at renewal time. Your health needs and medical costs change every year.

The Bottom Line

₹5 lakh health insurance is not enough in 2026. It may have been an adequate starting point a decade ago, but the combination of medical inflation, rising hospital charges, complex lifestyle diseases, and longer life expectancy has made it dangerously inadequate for most Indian families.

The good news is that upgrading your coverage is more affordable than ever, thanks to the availability of super top-up plans and competitive pricing in the health insurance market. Spending an additional ₹500–₹1,500 per month on enhanced health insurance is one of the smartest financial decisions you can make today.

Do not wait for a hospital bill to teach you this lesson. The time to act is now, when you are healthy enough to qualify for better coverage and financially stable enough to afford it comfortably.

Your health is your most valuable asset. Insure it accordingly.